The Indian Smartphone Revolution: Paytm’s Coming of Age IPO!

A few weeks ago, I valued Zomato, the Indian online food delivery company, just prior to its IPO, and argued that the excitement about its potential was tied to the potential for growth in India and the shifting habits of Indian consumers. Since its public offering, Zomato’s stock price has reflected that excitement, more than doubling from its offering price of 74 rupees per share. Waiting in the wings for its public debut, is Paytm, a company that in many ways is even more closely tied to India’s macro story, drawing on the growth of online commerce in India and a willingness of Indian consumers to use mobile payment mechanisms. In this post, I will look at the levers that drive Paytm’s value, and you can make your judgments on where you think this offering will lead in terms of valuation and pricing.

Setting the Table

As the Paytm IPO speeds to offering date, it is worth looking back at its relatively short history as a company, and how much change has been packed into that period. Since so much of Paytm’s success has been driven by the rise if smart phone usage among Indian consumers, and the concurrent rise in mobile payments for goods and services, I will start with a review of that rise, before looking at how Paytm has put itself in position to take advantage of that market shift.

The Rise of the Indian Smartphone User

India was late to join the smart phone party, held back both by the relative expensiveness of these devices, as well as the absence of affordable and reliable cell service in much of the country. In 2010, fewer than 2% of Indians had smart phones, with most of them being well off and living in urban areas. In the decade since, that has changed, as the smart phone market has exploded to reach hundreds of millions of Indians in 2020.

|

| Source: World Bank Database |

Entering 2021, more than 500 million Indians had smart phones, making it the second largest smartphone market in the world (after China), but its penetration rate of less than 50% of the market gave it more room to grow. There are multiple forces that have contributed to this shift, but two stand out.

- The first is that the costs of smartphones have decreased, and especially so in India, as technology and competition have worked their magic. In particular, the entry of Chinese brands, with Xiaomi and Vivo leading the charge, played a major role in making smartphones more affordable to Indians.

- The second is that cell service costs have also dropped, and in India, the drop in costs has been precipitous, after Reliance Jio entered the game in 2016, and quickly acquired 100 million subscribers by offering free voice and data calls over its 4G network. Today, Jio has more than 400 million subscribers, and while it remains a lightning rod for criticism, it is undeniable that it has played a major role in the evolution of the market.

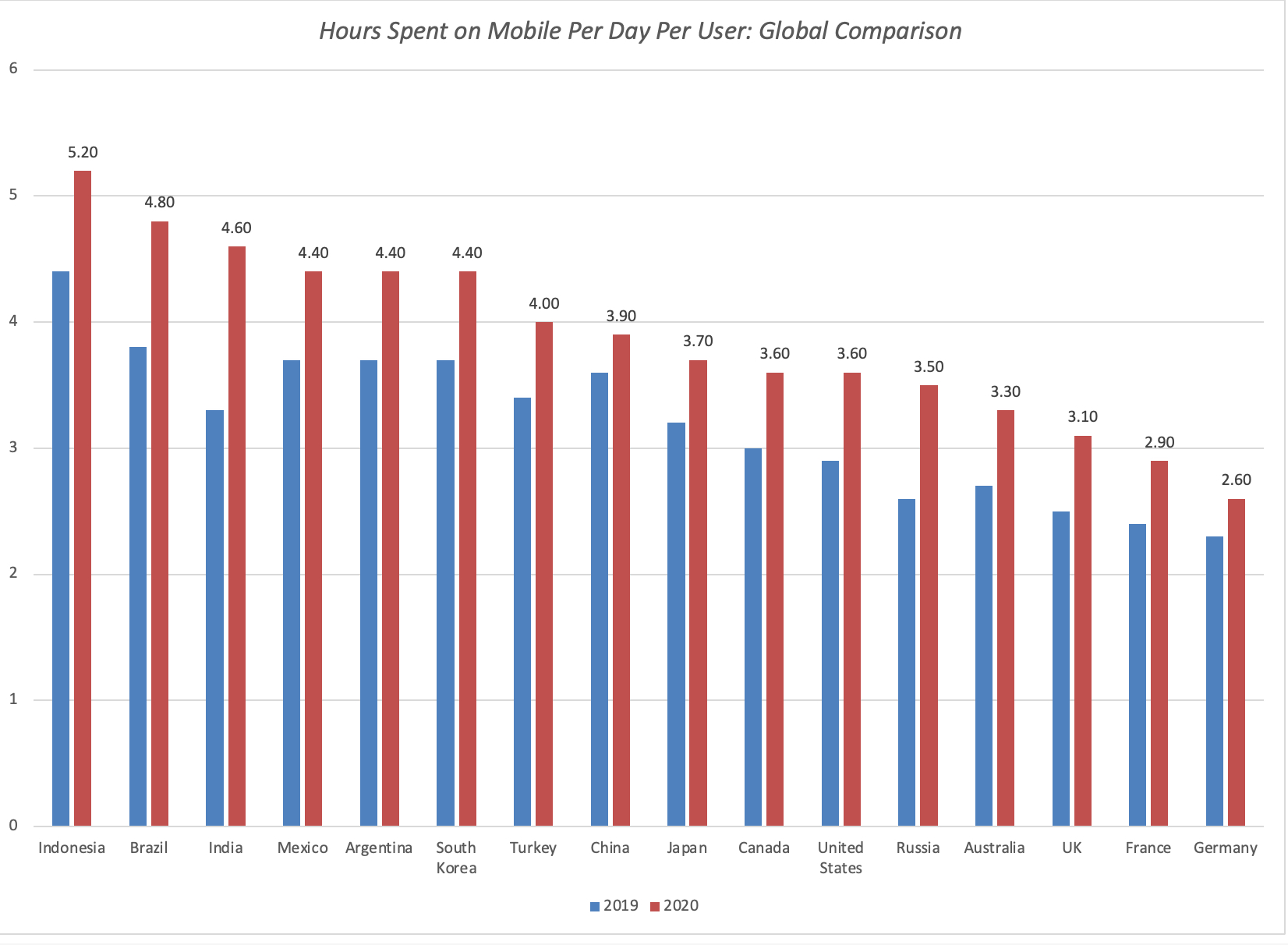

As smart phones have become ubiquitous in India, their usage has soared, partly because they are the only digital devices that many Indians have available to them to get online, and thus use to access social media, entertainment and shopping. By 2020, Indians ranked third in the world in how much time they were spending per day on their phones, with COVID contributing to a surge in that year:

|

| App Annie, State of Mobile 2021 |

Access to these smartphones, in conjunction with poor banking outreach in India, has created the perfect storm for a surge in mobile payments in India, and this graph bears out this trend:

|

| S&P, 2020 India Mobile Payments Market Report |

Within the mobile payment space, there was also an external development that added to its acceleration, and that was the advent, in 2016, of Unified Payments Interface (UPI), a real-time payment interface devised by the National Payments Corporation of India, and regulated by the Reserve Bank of India, facilitating and speeding up inter-bank, person to person and person to merchant transactions.

Paytm: Operating History

The rise of Paytm (Pay through Mobile) as a company parallels the rise of mobile phones in India. When it was founded in in 2010 by by Vijay Sharma, it operated as a pre-paid mobile platform, but its market then was small both in terms of numbers and services offered. As mobile access improved, Paytm has relentlessly added to its suite of products. In 2014, it introduced Paytm Wallet, a digital wallet that was accepted as a payment option by leading service providers and retailers. In 2016, it added ticket booking to movies, events and amusement parks, with flight bookings soon after, and started Paytm Mall, a consumer shopping app, based upon Alibaba’s Taobao Mall model. In 2017 it added Paytm Gold, allowing users to buy gold in quantities as little as 1 rupee, and Paytm Payments Bank, a messaging platform with in-Chat payments. In 2018, it added a Paytm Money, for investment and wealth management, and in 2019, it launched a Paytm for Business app for merchants to track payments. In short, over time, it has used its platform of users to launch itself into almost every online activity. As Paytm’s product suite has expanded, its numbers reflect both its strengths and weaknesses, with four key statistics tracking its expansion.

- The first is the number of users on its platform, using one or more of its many services.

- The transactions that these users make on the platform plays out in the gross merchandise value of all the products and services bought.

- The third is the take rate, i.e., the percentage of this gross merchandise value that Paytm records as its revenues.

- The last is the operating margin, it operating income (or loss) as a percent of operating income each year.

The table below is my attempt to recreate how Paytm has performed on these key measures in recent years, with the caveat that some of the information (on users and GMV, especially prior to 2019) is cobbled together from claims by corporate executives, press reports and opaque disclosures from the firm.

|

| Take Rate = Revenues/ GMV |

Looking at the numbers, we start to get a picture of Paytm, warts and all, over its lifetime. First, it is a growth company, if you define growth as growth in user count and number of transactions done on its platform, and perhaps in gross merchandise value. However, its growth in revenues has not kept track with those larger statistics, leading to a cynical conclusion that the company is adding new services and giving them away for nothing (or close to it) to pad its user/transaction numbers. Second, this is a company that seems to run on hyperbolic forecasts from its founders and top management, that are not just consistently higher than what the company deliver, but often by a factor of three or four. For instance, just to pick on one of many examples, Vijay Sharma claimed in an interview in 2019 with Business Standard that the company’s GMV would be $ 100 billion (7500 billion rupees) by the end of the year, more than double what the company reported as GMV for that year or the next. Third, access to capital from its deep pocketed investors, especially Alibaba, seems to have made this company casual about its business model and profitability, even by young, tech company standards. In fact, there is almost never even a mention of profitability (or aspirations towards profitability) in any of the corporate soundbites that I was able to read. The picture that emerges of Paytm is that of a management that is too focused on racking up user numbers, and too distracted to care about converting those into revenues and profits, while making grandiose statements about its future. Using the corporate life cycle framework to assess Paytm, it resembles an adolescent with attention deficit issues, in its scattershot approach to growth and absence of attention to business details, and if you are an investor, you have to hope that going public will cause it to grow up quickly.

Paytm: Funding and Ownership

Paytm’s ambitious growth plans have made it one of India’s premier cash burning machines, and it has been able to pull these plans off, because it has found ample sources of capital to feed them. In the table below, I list Paytm’s big capital infusions over its lifetime:

Along the way, there have been others who have provided capital to the firm (Reliance, Ratan Tata) who have exited as foreign investors, led by Alibaba and SoftBank, have muscled their way into the firm. Those capital infusions have naturally led to a diminution of the share of the company held by its founder, and the pie chart below lists the owners of Paytm, ahead of its IPO:

|

| Paytm Prospectus |

Note that while the company’s origins and business are in India, it is primarily a Chinese-owned company ahead of its IP0, with Ant Group, Alibaba and SAIF Partners (a Hong-Kong based private equity firm) collectively owning more than 50% of the shares, with the Softbank Vision fund as the next largest investor with 18%. Vijay Sharma’s holdings in the company have dwindled to 15% of the company, and his tenure as CEO depends on whether he can keep his foreign shareholder base happy.

Paytm: Story and Valuation

With that lead in, the pieces are in place to value Paytm and I will start by laying out the value drivers for the company and follow with my valuation. In making this assessment, I will draw on the company’s stated plans to raise money from the offering, though they may be altered as the company gets to its offering date.

The Story

The company’s history provides some insight into the Paytm’s value drivers, starting with a large and growing mobile payment market in India, and working down to the company’s operating metrics.

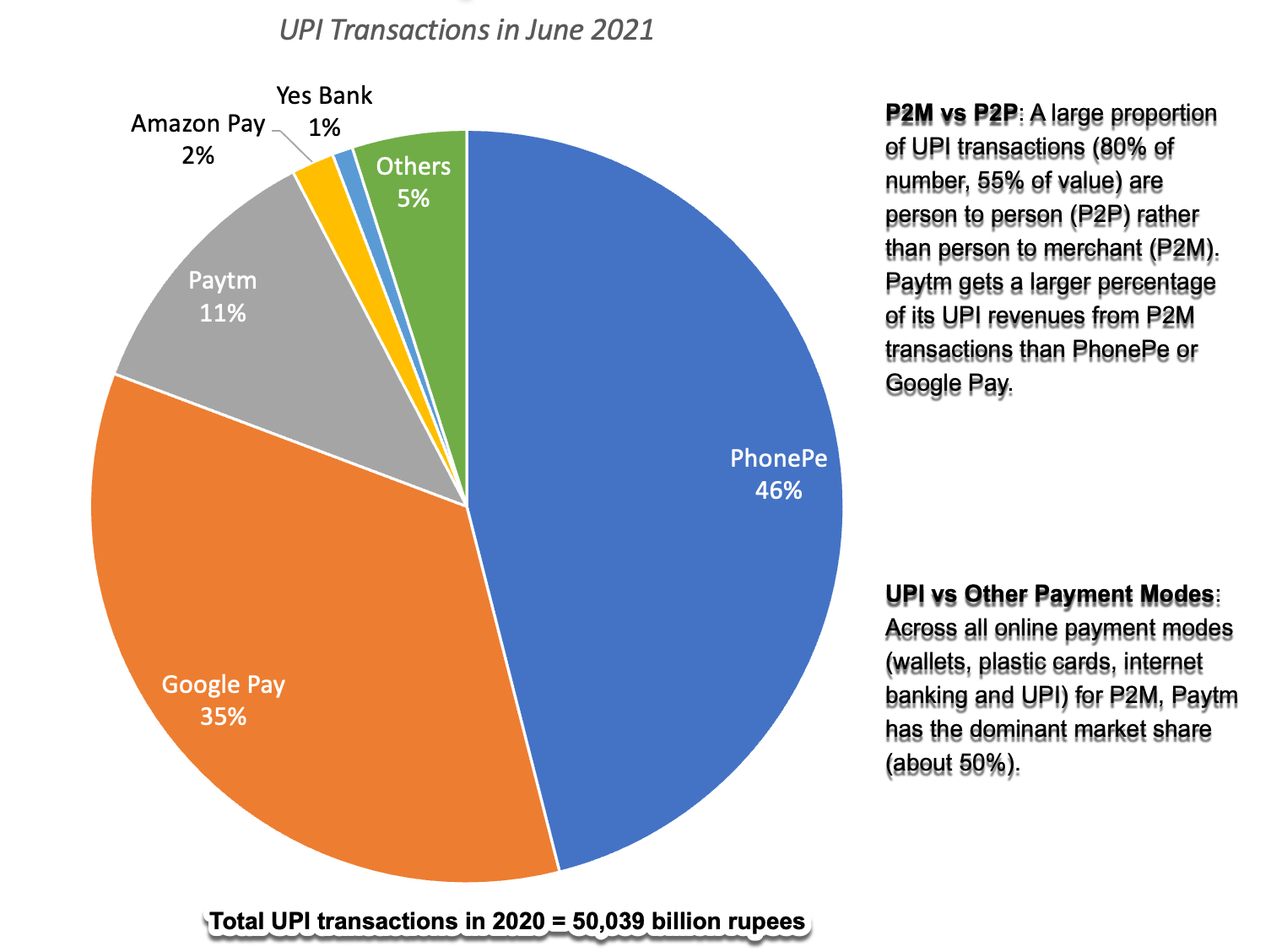

The value story for Paytm starts with a large and growing digital payment market in India, one that has surged over the last four years, and is expected to increase five-fold over the next five years, as the smart phone penetration rate rises for India and more merchants accept mobile payments. While Paytm has the advantage of having been in the Indian mobile payment market the longest, and having the largest user base, PhonePe and Google Pay have outmaneuvered Paytm in the UPI app ecosystem, claiming the lion’s share of that market, though the bulk of the transaction in that ecosystem are person-to-person. Paytm’s large user base, close to 350 million, and the wide acceptance of its wallets allow it to dominate the person to merchant (P2M) market in India, giving it a market share of close to 50% in early 2021.

The growth in the Indian mobile payment market will provide enough of a tailwind for Paytm to continue to grow its user base and transactions, but the bigger challenges for Paytm will be on the business dimensions where it has lagged in the past.

- The first is in the take rate, where Paytm has seen its revenue share of GMV drop from 2.18% in 2016-17 to 0.79% in 2020-21, as the company has prioritized acquiring users and user transactions over actually generating revenues from these transactions. To get a measure of a reasonable take rate that the company can aspire to reach in the long term, I looked at larger, more established players in the payment processing space:

|

| From company 10Ks. Removed net interest income from Amex revenues and subscription/bitcoin/hardware revenues from Square revenues |

Visa and Mastercard, the status quo players, still retain considerable market share, though Mastercard has a higher take rate (1.83%) than Visa does (1.11%); American Express has a higher take rate than the two larger players, because it gets a higher percent of its revenue from annual card fees. Paypal Shopify and Square, all of which derive their revenues from merchandising value, have take rates between 2% and 3%, though Square gets substantial additional revenues from bitcoin transactions (not counted in GMV or revenues in this table). Ant Financials, perhaps the company that Paytm has most closely modeled itself around, has a low take rate (1.37%), but makes up for it with huge transaction volumes. In modeling Paytm’s take rate over time, I will begin by assuming that the company will spend the next few years putting user growth first, at the expense of generating revenues, and that the take rate will stay low over the next five years, rising slowly to 1% in 2026. In the years following, though, I expect the take rate to double (to 2%), as the focus shifts from users to revenues, and its business model approaches that of a more conventional payment processing company.

- The second big challenge that Paytm faces is generating profits, a feat the company has been unable to accomplish over its lifetime. While the operating margins posted by Visa and Mastercard may be unreachable, note that Paypal’s operating margin has been trending up, as the company has become bigger. As Paytm increases its revenues, and user growth starts to level off, Paytm’s marketing and personnel expenses should start to decrease, and I expect operating profits to turn positive and the operating margin to reach 5% in 2026, and for that improvement to accelerate in the following five years, as growth rates decrease, allowing for an operating margin of 30% in stable growth.

- As a technology company, whose most valuable asset is the platform that it offers and products and services on, Paytm’s reinvestments have been mostly in the form of acquisitions and technology investments, and we assume that it will continue to follow this path, generating ₹3 in revenues for every rupee of capital invested in the near term, but ₹2.45 per dollar invested in the long term, converging on an industry average (for business and consumer services). Within the online payment space, this number has wide variance, with Paypal, perhaps the most mature of the companies, having a sales to invested capital of 2.54 over the last five years and Square, a younger and faster growing player, reporting a sales to invested capital of 5.68.

- On the risk front, there is little reason to reinvent the wheel. Paytm’s cost of capital, in rupee terms, is 10.43%, reflecting its business risk, and puts the company just below the median Indian company, in risk terms. The company’s capacity to burn cash will continue to expose it to risk, but with deep pocketed investors (Alibaba and Softbank), and a large cash balance (post IPO), the risk of failure is low (5%).

- To get from these numbers to a value per share, I use the existing share count, in conjunction with the information in the prospectus that the company plans to raise ₹16,600 million at the offering, with half of these proceeds staying in the firm to cover future investment needs and the other half going to existing shareholders, cashing out.

There are other Paytm businesses that may augment revenues in future years, but each one comes with caveats. The money deposited in Paytm wallets by users can potentially earn interest for the company, but restrictions that this money be kept in escrow accounts at banks, not always paying close to market interest rates, can crimp that income stream. Paytm Bank could expand from its very limited presence now to more traditional banking (taking deposits, making loans), but that is a capital and regulation intensive business. I believe that Paytm’s core value comes from being an intermediary, in the payments business, and the story reflects that belief.

The Valuation

If you buy into my story of Paytm continuing to maintain a dominant market share of the mobile payment market in India, while also increasing its take rate over time and improving operating margins to those of an intermediary business, you have the pieces in place for a valuation of Paytm, captured in the picture below:

|

| Download spreadsheet; Price per share of ₹2950 is for unlisted shares. |

I know that there are many on both sides of the value divide who will disagree with me on my story and valuation, and that is par for the course. On one side, there will be some who view a value of close to $20 billion (₹1500 billion) for a company with a pittance in revenues, a history of operating losses and distracted management as insanity. On the other side, there will be some who feel that I am not giving the company credit for all of the new businesses it can enter, using its vast platform of users, and thus under valuing the company. To both sides, my defense is that this is my story and valuation, and it will drive my investment, but that you are welcome to download the spreadsheet, change the inputs that you disagree with and come up with your own valuations.

In making my assessment, I fully understand that there is substantial operating and execution risk in this story, since this value presupposes that Paytm will remain a dominant player in the Indian mobile payment space, as it grows, and that Paytm’s management will pivot from growing users to growing revenues and from growing revenues to growing profits, over time, with nothing in their history to back that up. Needless to say, if I invested in Paytm, it would not only have to be at the right price, i.e., trading at less than ₹1500 billion, but also with the acceptance that this cannot be a passive (buy and hold) investment, but one that will require active engagement and monitoring of the company’s actions and performance. To assess how this uncertainty will play out in my estimates of overall equity value, I did a Monte Carlo simulation, with my point estimates on total GMV, take rate, operating margin and sales to invested capital replaced with distributions:

|

| Crystal Ball used for simulation |

There are lessons, albeit some obvious, that emerge from this simulation. First, given that almost all of the value of Paytm comes from expectations of the future, and there is significant uncertainty on every single dimension, it should come as no surprise that the range on estimated value is immense, with a 3%chance that the company’s equity is worth nothing to more than ₹2000 billion at the 90th percentile. Second, with this range in value, the potential for your priors and biases to play out on your final valuation are strong. Put simply, if you like the company so much that you want to buy the stock, you can find a way to make the assumptions that get to that value. Third, even if you strongly favor the company and find it under valued, it would be hubris to concentrate your portfolio, around this stock. In other words, this is the type of stock that you would put 5% or perhaps 10% of your portfolio in, not 25% or 40%.

Closing Thoughts

As human beings, it is natural for us to categorize choices we face into broad groupings, because those groupings then allow us to generalize. In the 1980s, when technology companies first entered the market in big numbers, we classified them all as high growth, high risk investments. While that categorization would have worked at the time, it is quite clear that the technology sector today is not only a dominant segment of the market (accounting for the largest slice of the S&P 500 market capitalization pie), but is also home to a wide array of companies. In fact, at one end of the spectrum, there are many older tech companies that are now mature, and perhaps even in decline, and several are stable, cash earning machines, akin to the consumer product companies of the 1980. At the other end, you see new sub-segments of technology-based companies that have emerged to claim the “high growth, high risk” mantle, deriving more of their value from the number of users on their platforms, than from conventional financial metrics. A few weeks ago, when I valued Zomato, I argued that it was a joint bet on the company’s continued dominance of the food delivery market and the growth in the Indian restaurant/food delivery business. Paytm is also a joint bet on an early entrant into the Indian mobile payment market, continuing to maintain market share, in a growing digital payment market in India. That said, the companies have very different business models, with Zomato’s 20% plus take of every dollar spent on its platform vastly exceeding Paytm’s less than 1% take of every dollar spent on its platform. They are both big market bets, but the Paytm bet is much more dependent on management figuring out a way to grow, while improving take rates at the same time.

YouTube Video

Spreadsheets to download